Nautilus: Growth at 1x Sales

Deep-dive on longstanding industry leader in health & fitness products, Nautilus. Investment thesis predicated on their digital transformation.

- Nautilus is a longstanding industry leader in health and fitness products

- Financials and current valuation indicate a potential market inefficiency which should lead to long-term stock price appreciation

- New key executives & directors are accelerating the company’s digital transformation

- Health and fitness market continues to grow

- COVID-19 indefinitely accelerated demand for at-home fitness solutions

Profile

Nautilus designs, develops, sources, and markets cardio and strength fitness products, and related accessories for consumer and commercial use globally.

Product mix

The company sells its products under the following brands:

- Nautilus

- Schwinn

- Universal

- Bowflex

The Nautilus brand sells upright and recumbent bikes, ellipticals, and treadmills starting at $399.

The Schwinn brand sells indoor cycling, airdyne, recumbent, and upright bikes, ellipticals, treadmills, rowers, and accessories.

The Universal brand sells adjustable dumbbells, kettlebells, benchs, upright and recumbent bikes, and ellipticals.

While these various brands provide diversification and exposure to different demographics, Bowflex appears to be Nautilus’ long term growth winner. Bowflex sells a variety of the following high-end fitness products: Bikes, Max Trainers, Home Gyms, SelectTech, Treadmills, accessories, and the JRNY software.

Just in the last 3 months, Nautilus bolstered their Bowflex product portfolio by launching four new cardio products all integrated with the JRNY fitness platform (New C7 bike, two new treadmills, and an updated Max Trainer).

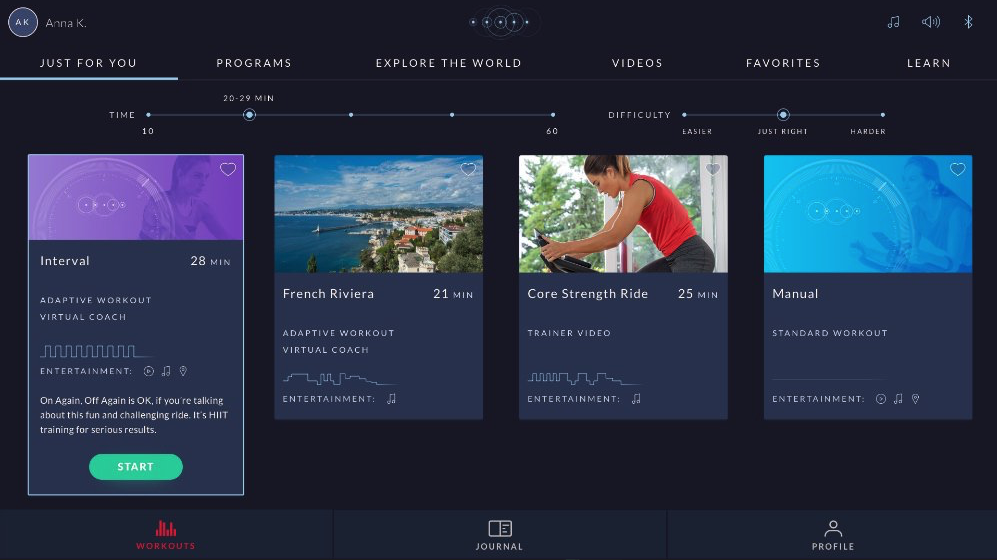

JRNY

JRNY is Nautilus’ new interactive fitness software. The platform uses machine learning that delivers personalized experiences for users. All new Bowflex products come “JRNY enabled” meaning they operate on JRNY software.

JRNY user interface is outstanding. Whether you’re using the product’s touchscreen, your phone, or tablet, the software runs seamlessly. The front page is “Just for you” (your user) and the AI is spot on in regards to tailored workouts.

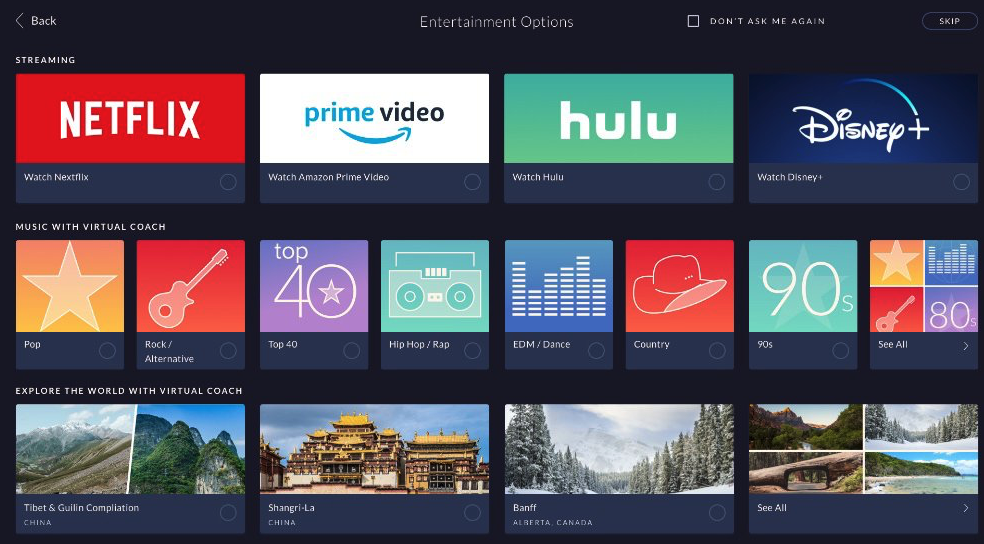

Upon selecting a workout, the user is given a wide variety of entertainment options to go alongside their workout. These options include video streaming from your favorite apps, Bowflex Radio, or exploring countless destinations around the world with your virtual coach.

The new JRNY enabled cardio machines come with a 2-month free trial then auto bill $20/month (or $12.42/month for annual membership). I think a 60-day free trial should be music to investors' ears. Why? Put yourself in a user’s (cycling) shoes. You’ve just purchased a new JRNY enabled VeloCore bike. You spend your first few days trying out various programs and entertainment features. During this time, you’ve established preferences. For example, you prefer high-intensity interval training with a virtual coach while watching Netflix. You’ll then spend the next 60 days establishing a workout routine. Every morning, after checking the news, you clip into your VeloCore, habitually select your daily recommended 30 minute high-intensity interval training program, and select Netflix as your entertainment option. According to Healthline, it takes an “average of 66 days for a new behavior to become automatic”. You just spent the last 60 days teaching your Prefrontal Cortex and hippocampus to automate these actions. Inevitably once your JRNY free-trial concludes and you’re forced to pay $20/month or completely change your workout preferences - What would you do?

Since investors don’t have access to JRNY subscriber data just yet, we can only infer that new users who purchased a JRNY enabled cardio machine will want to continue using the feature-rich software due to its clear added value for home fitness.

Not only does JRNY create a massive value add for its users, it generates a new (sticky) revenue stream for Nautilus, collects valuable user data, and continues to improve through machine learning.

If they continue to execute in the SaaS space, JRNY could be Nautilus’ ticket to being valued as the growth company it really is. Subscription based recurring revenue is significantly more valuable than one-time transactional sales and Nautilus is making a commendable effort in shifting their focal point from hardware to SaaS.

Now that Nautilus’ product mix is understood, let’s dive into their financials.

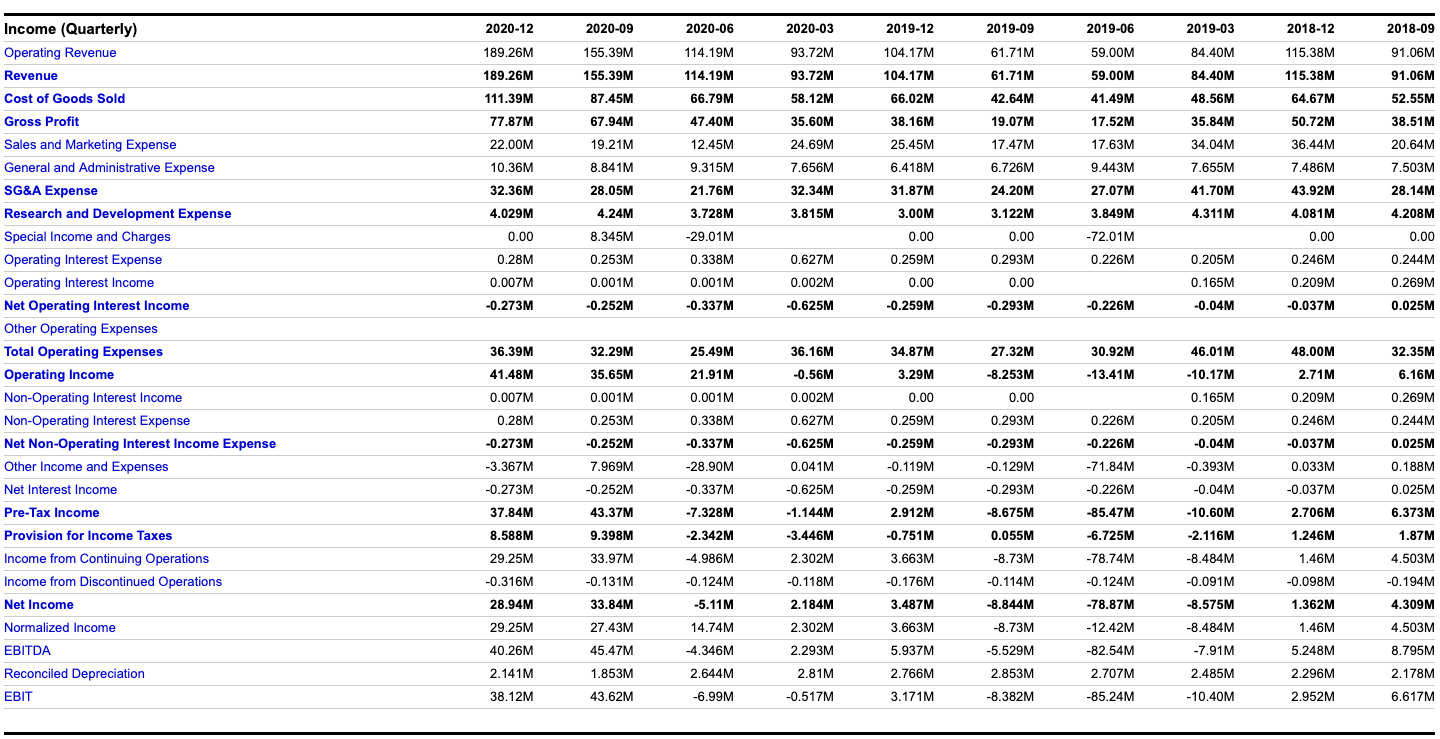

2020 Earnings Recap

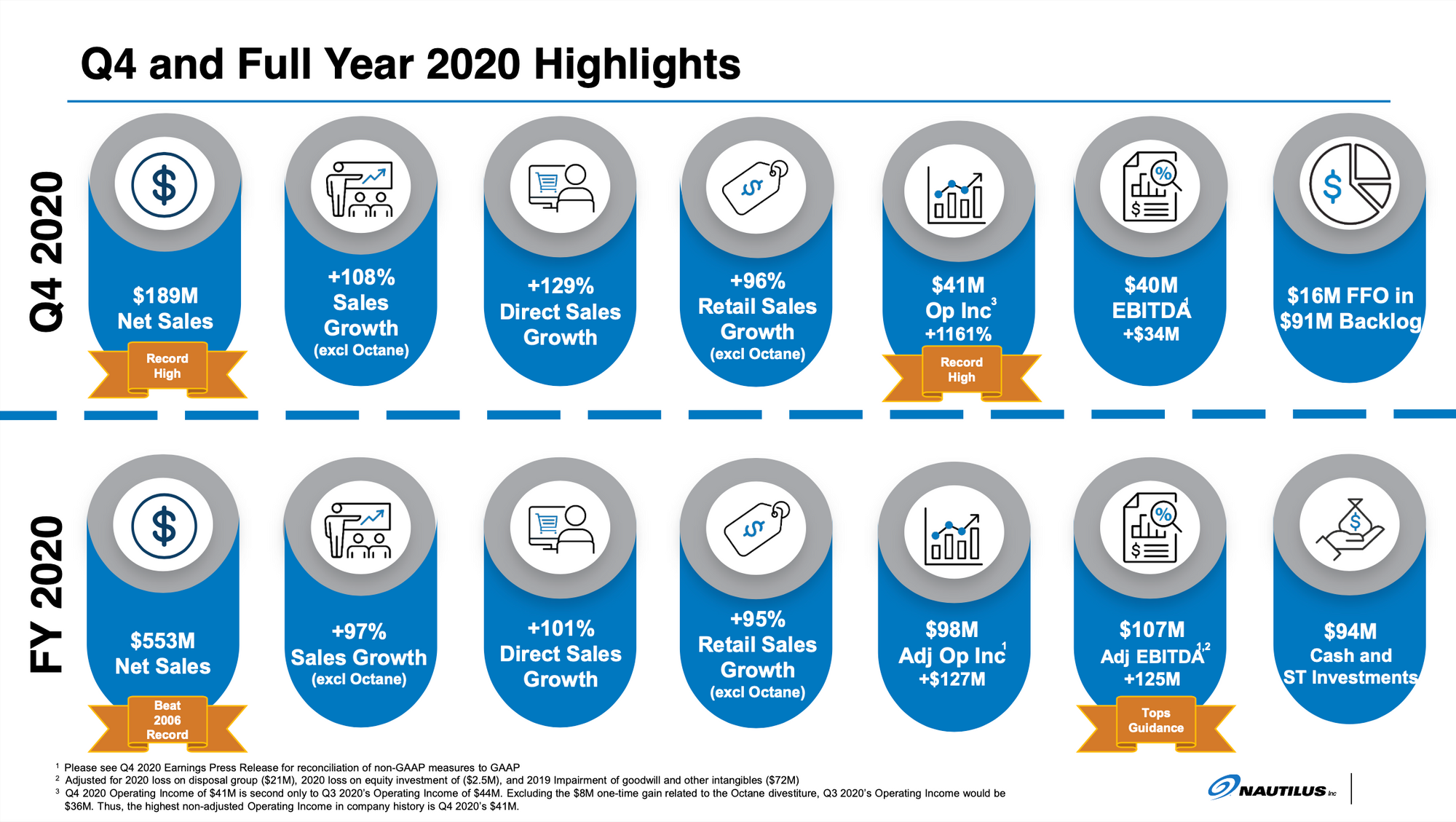

Q4 2020 vs. Q4 2019 (CEO Jim Barr took over in 07/19):

- Net sales: $189.3 million (+108% excluding sale of Octane brand)

- Direct to consumer: cardio sales +78%, strength product sales +372%

- Retail: cardio sales +59%, strength product sales +53%

- Gross profit: $77.9 million (+104%)

- Gross margin: 41% (+4.5%)

- Increased full-priced selling in direct to consumer segment

- Improved wholesale margins and fixed cost leverage in retail

- Above was partially offset by increased transportation costs driven by COVID-19 logistics disruptions

- Operating income: $41.5 million compared to $3.3 million last year (+$38.2 million)

- Net Income: $28.9 million (or $0.89 per diluted share) compared to $3.5 million (or $0.12 per diluted share) last year (+730%)

You may be asking yourself: If Q4 was so strong, why did NLS sell-off the following day? Revenue was within management’s guidance, but fell $1.4 million short of consensus (reported $189.3 million vs. consensus of $190.7 million). Coming in short of revenue consensus was undeniably through no fault of their own. There was a severe shortage of shipping containers at the time. In fact, “At year-end, we (Nautilus) had over $16 million of completed and sold inventory, sitting near our factories, just waiting for retailers to pick them up.”

“Under the factory fulfilled orders arrangement, retailers are responsible for arranging transportation, finding containers and picking them up at our factory at which point title passes and our revenue is recognized. When even leading retailers like Amazon are not able to take possession of product they badly want, due to an inability to find shipping containers, it serves as a strong illustration of the global disruption that occurred.” - Jim Barr, CEO

So, let’s see what their revenues would have looked like if the orders were picked up as scheduled:

Reported revenues ($189.3 million)

+ orders sold and ready to be picked-up by retailers ($16 million)

= $205.3 millionReporting $205.3 million in revenue for Q4 would have represented an +8% beat over consensus.

For this reason among others, investors should perceive the post Q4 2020 sell-off as a buying opportunity.

All told, Nautilus entered 2021 with sales backlog of $91 million.

FY2020 vs FY2019 (CEO Jim Barr took over in 07/19):

- Net sales: $552.6 million (+97.2% excluding sale of Octane brand)

- Direct to consumer: cardio sales +83%, strength product sales +186%

- Retail: cardio sales +67%, strength product sales +61%

- Gross profit: $228.8 million (+107%)

- Gross margin: 41% (+5.6%)

- Operating income: $77.8 million compared to last year’s loss of $100.5 million (+$178.4 million)

- Net income: $59.8 million (or $1.86 per diluted share) compared to last year’s loss of $92.8 million (or -$3.13 per diluted share)

- Liquidity (year end 2020 compared to year end 2019):

- Cash & cash equivalents: $94.1 million compared to $11.1 million

- Debt: $13.5 million compared to $14.1 million

Furthermore, the company informed investors of growth in the following metrics:

- 4x increase in new customers

- 4x increase in web traffic to schwinnfitness.com

- 3x increase in web traffic to Bowflex.com

- 4x increase in media impressions

I’ve attached an aggregated copy of Nautilus’ quarterly Income Statements from 2018-2020 to highlight the dramatic turn of the tide.

Looking forward, Nautilus expects Q1 2021 net sales growth between 50-75% versus the same period last year. This should assure investors that consumer demand for at-home fitness solutions will continue past 2020.

Valuation

(The following data was collected on March 3rd, 2021)

- Market cap: $582 million

- Revenue (TTM): $553 million

- Revenue Growth (YOY): 92% (excluding sale of Octane Brand)

- Gross Margin: 41%

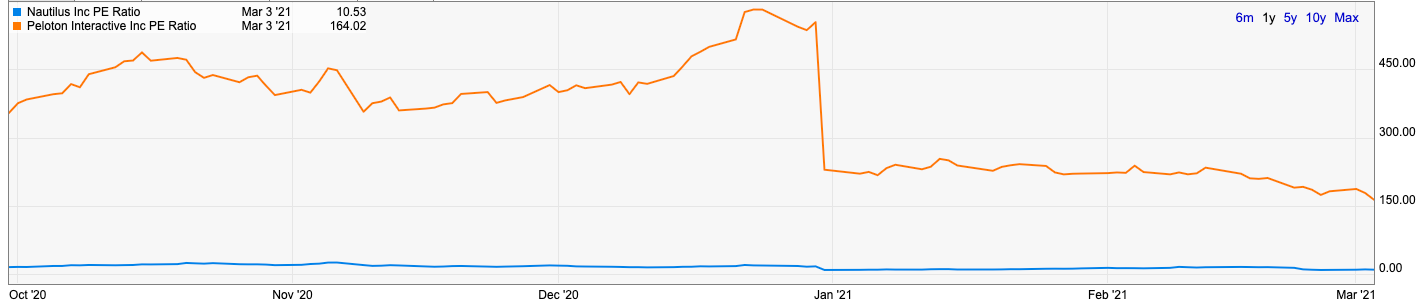

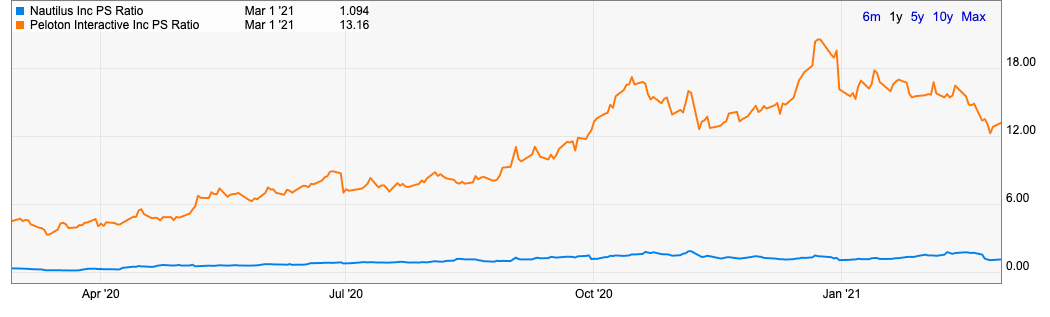

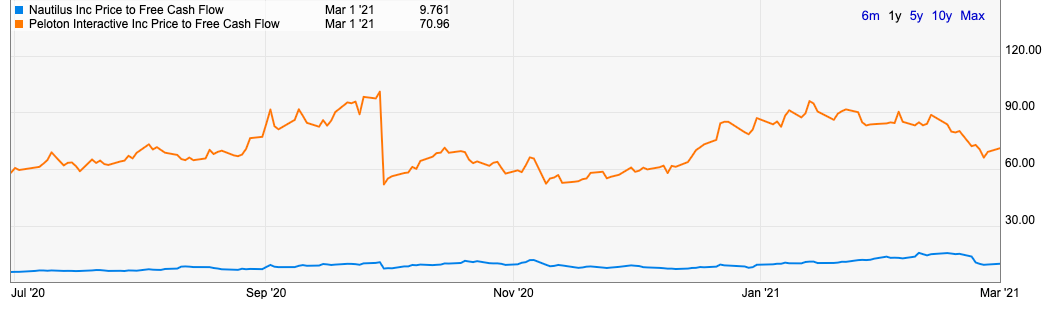

With questions of valuation surrounding U.S. equities in 2021, let’s analyze a few key financial ratios and compare them to Nautilus competitor, Peloton ($PTON).

Price-to-earnings ratio (PE):

- Nautilus: 10.53

- Peloton: 164.02

Price-to-sales ratio (PS):

- Nautilus: 1.09

- Peloton: 11.50

Price to free cash flow:

- Nautilus: 9.76

- Peloton: 70.96

Now that we’ve resolved potential valuation concerns, let’s examine the professional backgrounds of the new execs Jim Barr brought to the team in the past 18 months.

New Key Executives and Directors

James (Jim) Barr, CEO Joined Nautilus, Inc. as Chief Executive Officer and Board Member in July 2019. He brings with him key capabilities of driving growth through people leadership, consumer-driven marketing, innovation and technology, as well as multiple successes transforming and growing large scale digital and multichannel businesses in diverse industries. Before joining Nautilus, Inc. Mr. Barr was Group President of Ritchie Bros., a global leader in the sales of used industrial equipment. Prior to that Mr. Barr held the position of EVP and Chief Digital Officer of OfficeMax where he led the transformation of its online and omnichannel experiences. In 2008, Mr. Barr was named the first President of Sears Holdings’ newly-formed Online Business Unit, where he developed and drove an omnichannel and online strategy that rapidly expanded the product assortment and growth. Mr. Barr’s foundational digital experiences came as an executive for 12 years in Microsoft’s online businesses as GM, Commerce Services, where he led Microsoft’s B2C ecommerce businesses, such as online shopping, classified advertising and auctions, as well as underlying technology platforms.

Aina Konold, CFO Named Chief Financial Officer in December 2019. To this role Aina brings over 25 years of financial management experience and a deep knowledge of consumer goods. Prior to joining Nautilus, Inc., Ms. Konold held several executive level finance positions during her 20-year career with Gap, Inc., including senior leadership roles across financial planning and analysis, real estate strategy, and investor relations. Most recently, she was the founding CFO for Gap Inc. in China where she grew store count from four stores to more than 175. During her tenure the business experienced rapid revenue growth and established a business model to achieve profitable growth. Ms. Konold was also instrumental in creating practices that enabled sustainability in a constantly evolving marketplace, particularly in the areas of digital and e-commence. Konold graduated from Stanford University and began her career at PricewaterhouseCoopers.

Becky Alseth, VP of Marketing Joined Nautilus, Inc. as Vice President of Marketing and Direct in March 2020, and in February 2021 strategically transitioned to VP of Marketing. In her role, Ms. Alseth leads the Direct to Consumer business, as well as marketing for the Company. Prior to joining Nautilus, Becky held senior marketing and branding positions at Fortune 500 companies including Avis Budget Group and The Clorox Company, as well as global giants, Diageo and Nestle, with repeat successes of growing market share, customer loyalty and brand equity.

Ellen Raim, CPO Named Chief People Officer (CPO) in March 2021. She oversees HR strategy and leads Nautilus, Inc.’s business growth through the lens of people where her focus is on recruitment, succession planning, learning and career development, diversity and inclusion, organizational effectiveness, employee engagement, pay and benefits, and employee relations. Prior to joining Nautilus, Inc. Ms. Raim was Vice President, People and Culture, at Invoca, a software start-up, where she built the “people systems” to enhance and protect the culture as the company scaled. She began her career as a labor and employment attorney for a large multinational law firm, moved into Human Resources at Intel Corp. and held many positions there with worldwide scope. After Intel, she held roles as Vice President of Human Resources at several high-tech hardware companies. Ms. Raim holds a B.A. in Economics from Brown University, an M.A. in Organizational Design from Seattle University, a Masters in Behavioral Science from London School of Economics, and a J.D. from the University of Miami School of Law.

Garry Wiseman, VP & CDO Named Senior Vice President and Chief Digital Officer in October 2020. Mr. Wiseman brings more than 25 years of product and e-commerce capabilities, as well as expertise in designing and implementing high scale digital experiences at some of the world’s largest technology companies, including Microsoft, eBay, Salesforce and Dell. Prior to joining Nautilus, Inc., Mr. Wiseman served as Senior Vice President of Digital Customer Experience for Dell Technologies where he steered the company through a rapid digital transformation that led to significant year-over-year revenue increases and enhanced performance. Wiseman was responsible for Dell.com, the Dell Premier B2B marketplace, all offline sales systems and in-house commerce platforms, as well as leading product management, design, engineering, and content teams. In his role at Nautilus, Inc., Mr. Wiseman oversees general management of JRNY and the Direct channel, and will help coordinate software and digital initiatives to accelerate the Company’s ongoing digital transformation. Mr. Wiseman attended Wolverhampton University and has authored eight US patents.

Now, some may argue that changes in management could be a negative sign. I couldn’t have been more pleased to see Jim Barr take over in 2019. As an e-commerce veteran, Barr is the perfect leader to steer Nautilus’ in the right direction. Additionally, his new executive hires can give investors an indication to where the company’s long term focus is: Improved people management, revamped marketing campaigns, increased direct to consumer sales, accelerating their digital transformation and continuing to raise the bar for Nautilus’ JRNY software.

Analyzing the Health and Fitness Market

One key factor driving health and fitness market growth is the heightened effort of individuals towards living healthy lifestyles due to the risks associated with unhealthy living. The rising consumption of unhealthy foods is a leading cause of obesity throughout the globe. According to the WHO, more than 1.9 billion adults were overweight during the year 2016 and more than 600 million were obese. Furthermore, the U.S. The Department of Health and Human Services states that the prevalence of obesity increased by 11.9% between the periods 1999-2017. Similarly, the prevalence of severe obesity reached 9.2% from 4.7% during the same period. The growing rate of obesity paired with the snowball effect of consumers striving towards living healthier lifestyles is significantly boosting the adoption of health and fitness hardware and software.

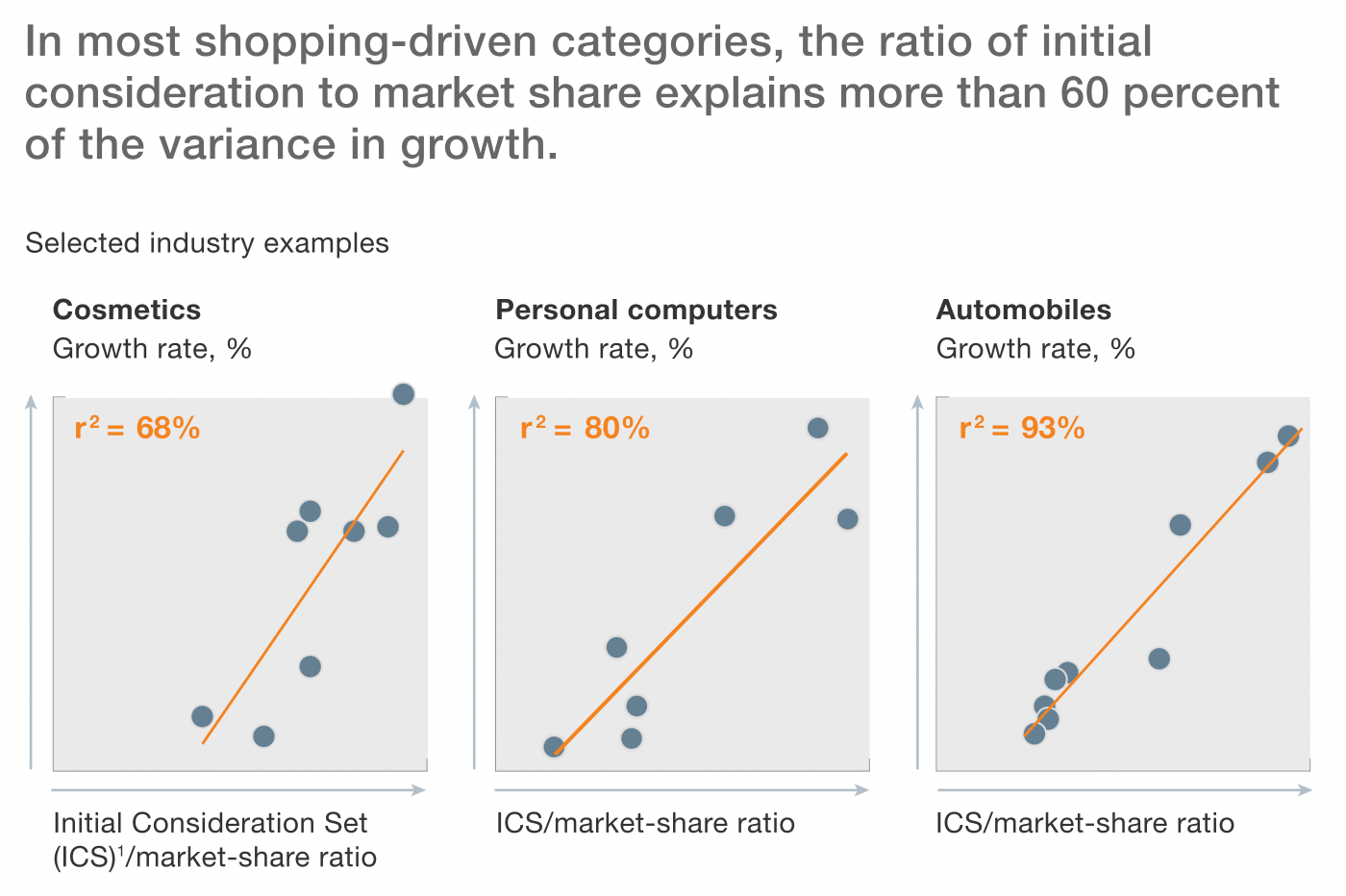

While these macro factors contribute to consistent growth in the health and fitness market, COVID-19 significantly accelerated the demand for at-home fitness solutions. With a strong product offering, Nautilus was a clear benefactor of the unexpected increase in demand. As indicated by exponential increases in web traffic, many consumers included Schwinn, Nautilus, and Bowflex products into their consideration set for at-home fitness products. This should position Nautilus ahead of new entrants into the connected fitness market as McKinsey's study on marketing-led growth found a strong correlation between initial consideration and growth in market share.

As the connected fitness market continues to grow: Peloton, Lululemon, NordicTrack, and Bowflex are emerging as market leaders. However, Lululemon and Peloton are neglecting a a significant part of the total addressable market - consumers who enjoy connected fitness but can't justify shelling out $2500 for a single piece of equipment. This is where Nautilus has a leg-up above any competition. As an industry leader for decades, Nautilus offers state of the art equipment that competes with the likes of Peloton but also has a wide range of affordable options as well. In the coming years, Nautilus will benefit heavily from their diverse product offering as they scale their connected fitness platform across their various brands.

Large Caps and Mega Caps Racing for Market Share

Now, let’s see how a few large and mega cap companies are betting on the growth of the health and fitness market.

- Apple Watch

- Google’s $2.1B acquisition of Fitbit

- Google’s Project Nightingale

- Amazon’s Halo

- Apple’s Fitness+

- Lululemon’s Mirror acquisition

- Peloton’s Precor acquisition

- Apple’s latest job posting, Sr. EPM manager, will work in the Health Technologies team to “lead the design and development of Apple-branded Health Hardware products.”

We should expect more M&A in the health and fitness sector. At a market cap of <$1B Nautilus could be the beneficiary of an acquisition. That said, I’d prefer to see Jim Barr and his team continue to execute for a few years before any M&A speculation.

Potential Risks

Investing in Nautilus has inherent risks. The health and fitness industry contains fierce competition which could provide headwinds to Nautilus’ stock price. Each segment and product of Nautilus' business should be understood before investing in this company. Additionally, investors should acknowledge that COVID-19 accelerated Nautilus’ sales growth and led to significant stock price appreciation. If the forecasted demand for at-home fitness does not come to fruition, Nautilus’ stock price could decline.

Where to

Demand hasn't declined despite COVID-19 vaccine rollouts. Recent polling results show >20% of former gym-goers say they will never return to the gym while the rest say they will balance their gym and at-home routines differently than before COVID-19. Management expresses optimism that a portion of the current elevated demand will continue long term.

Nautilus’ latest product launches and JRNY 2.0 have received good coverage and glowing customer reviews, positioning them well for 2021.

On the Q4 2020 earnings conference call, Jim Barr announced the completion of North Star, their long-term strategy that “builds on the company’s well-known brands, reputation for quality and innovation, broad product portfolio, and consumer focused company culture.”

Nautilus ended the year with over $90 million in cash and short-term investments “providing additional resources needed to accelerate our North Star strategy and ultimately deliver sustainable long-term growth.”

The company will present the details of North Star alongside the release of JRNY subscriber data for the first time on March 18th, 2021. It is my firm belief that this upcoming investor day serves as a near-term catalyst to Nautilus shareholders.

Follow along if you're interested in learning about financial markets, innovative companies, and potential investment opportunities. You can stay up-to-date by subscribing, in order to get each post delivered to your email.